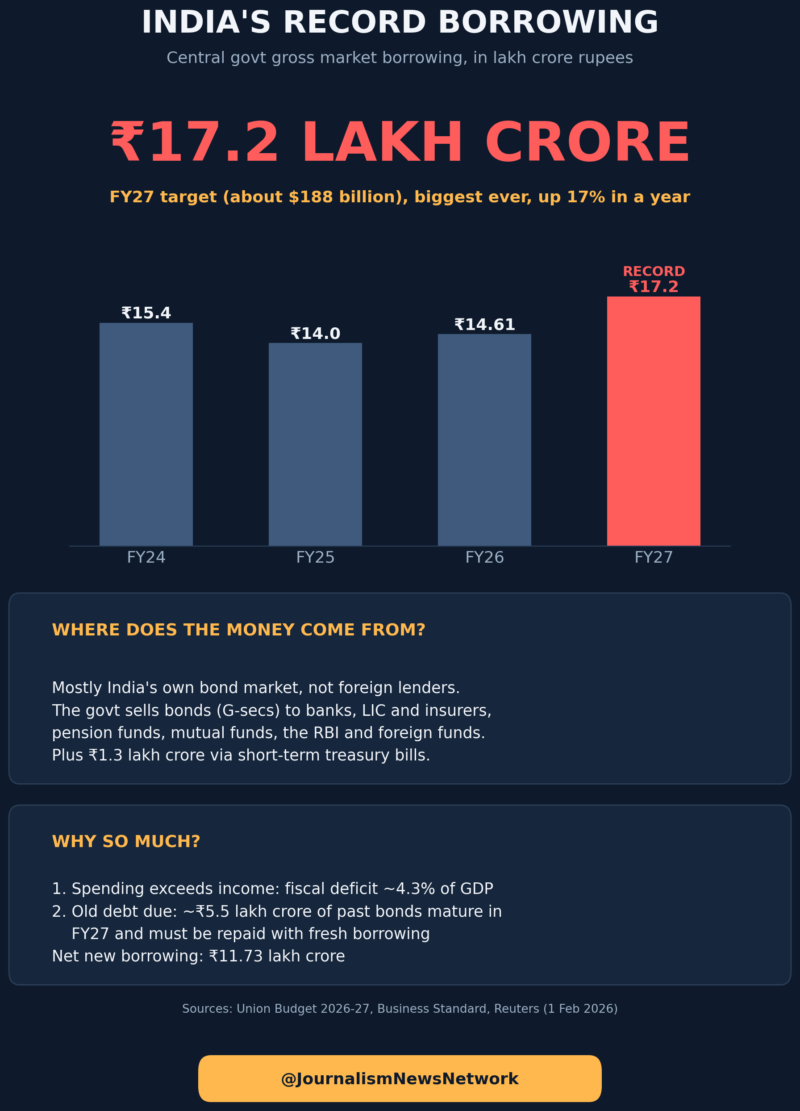

On 1 February 2026, Finance Minister Nirmala Sitharaman announced that the government will borrow a record ₹17.2 lakh crore (about $188 billion) from the market in FY27. That is 17% more than the ₹14.61 lakh crore borrowed in FY26, and higher than what most economists expected.

Where does the money come from?

Not foreign lenders. Mostly India’s own bond market. The government sells bonds called G-secs, and the buyers are Indian banks, LIC and other insurers, pension funds, mutual funds, the RBI and, increasingly, foreign funds. Another ₹1.3 lakh crore comes via short-term treasury bills.

Why so much?

Two reasons. First, the government spends more than it earns; the fiscal deficit target is around 4.3% of GDP. Second, roughly ₹5.5 lakh crore of old bonds mature in FY27 and must be repaid, so a big chunk of new borrowing just refinances old debt. Net new borrowing is ₹11.73 lakh crore

The chain reaction that hit banks

Here is the part most readers miss. When the government floods the market with bonds, lenders demand higher interest, so bond yields rise. The 10-year yield was already at 6.70% before the Budget.

And there is a golden rule in finance: when yields go up, the prices of OLD bonds go down. Nobody pays full price for an old bond earning 6.5% when new ones pay more.

Banks hold lakhs of crores in old bonds. When yields jumped, those holdings lost value, meaning losses on banks’ books. Investors did the math within hours. The day after the Budget, SBI fell 5.3% and the Nifty PSU Bank index dropped 5.6%

The bottom line

A record loan is not free. Its interest bill lands on future budgets, its bond flood pushes up borrowing costs for companies, and its first casualties were the bank stocks in your portfolio.

*Next in this series: the ₹2.2 lakh crore foreign exit.*